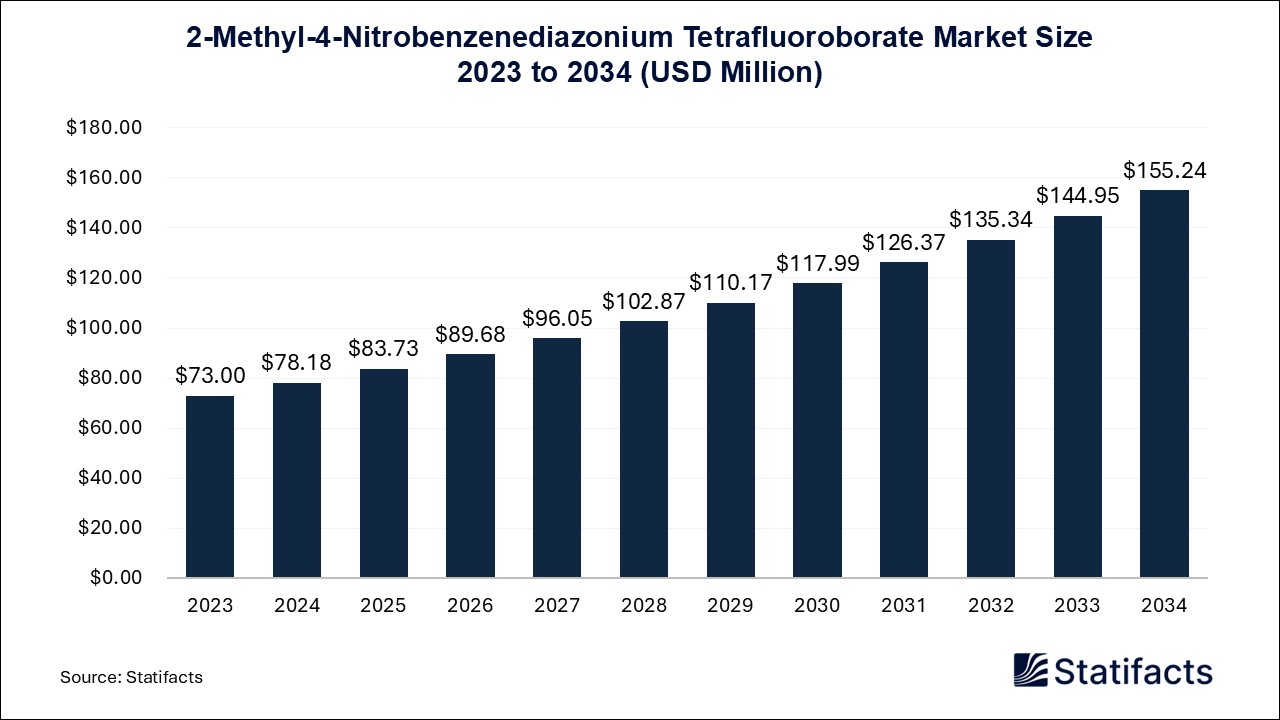

The U.S. closed system transfer device market size surpassed USD 492 million in 2024 and is predicted to reach around USD 1,287.77 million by 2034, registering a CAGR of 10.1% from 2025 to 2034.

The U.S. closed system transfer devices market is witnessing high growth with rising apprehensions regarding exposure to hazardous drugs in healthcare. Closed system transfer devices (CSTDs) are used to prevent the evaporation of hazardous drug vapors, minimize chances of contamination, and enhance employee safety. Enhanced usage of chemotherapy drugs, tight regulatory policies, and growing concerns regarding occupational risk are major market drivers. As medical facilities keep emphasizing worker protection and regulation adherence, CSTD demand will likely increase tremendously.

The growing cancer incidence in the U.S. has contributed to increased demand for chemotherapy agents, most of which are categorized as hazardous substances. Healthcare workers exposed to these drugs are at risk of exposure, which may cause serious health problems. CSTDs are important in reducing such risks through the provision of a closed system that does not allow for contamination. Increased cases of oncology treatments and chemotherapy sessions in hospitals and infusion centers directly are leading to the growth of the U.S. closed system transfer devices market.

Regulatory authorities like the U.S. Food and Drug Administration (FDA) and the United States Pharmacopoeia have introduced stringent guidelines for the safe handling of hazardous drugs. These guidelines require the use of CSTDs to safeguard healthcare professionals from exposure. Further, Occupational Safety and Health Administration (OSHA) and National Institute for Occupational Safety and Health (NIOSH) guidelines also highlight the necessity of protective devices. Adherence to these guidelines is fueling the extensive use of CSTDs in healthcare centers.

As the emphasis on workplace safety grows, hospitals and pharmacies are actively putting money into guard technologies such as CSTDs. Healthcare professionals are increasingly concerned with the hazards of handling dangerous drugs, thus creating a bigger market for minimizing exposure solutions. The harmonization of training programs and safety measures is further increasing rates of adoption within medical facilities, leading to future growth for the U.S. closed system transfer devices market.

| Industry Worth | Value |

| Market Size in 2024 | USD 492 Million |

| Market Size in 2025 | USD 541.69 Million |

| Market Size by 2034 | USD 1,287.77 Million |

| Market Growth Rate from 2025 to 2034 | CAGR of 10.1% |

Even with the advantages of CSTDs, their high cost remains a major limiting factor for adoption, especially among smaller healthcare centers with limited financial resources. CSTDs require sophisticated engineering and high-grade materials that drive their high prices. Moreover, meeting rigorous regulatory requirements increases manufacturing costs. Large hospitals and oncology centers have the financial wherewithal to undertake these investments, but smaller clinics and independent pharmacies can find it challenging to absorb the financial outlay, thus restricting overall U.S. closed system transfer devices market penetration.

Artificial Intelligence (AI) is increasingly contributing to optimizing the design and deployment of closed-system transfer devices. AI is also improving drug compounding safety with automated detection systems that identify potential leaks or compromises in drug transfers. Data analysis through AI is also facilitating the monitoring of exposure levels and enhancing workplace safety procedures for healthcare professionals. As the process of AI integration advances, the effectiveness and uptake of CSTDs in the U.S. healthcare industry are likely to grow.

The increasing home-based chemotherapy and infusion therapy trend is a major opportunity for CSTD producers. With an increasing number of patients choosing home treatment, demand for safe drug transfer solutions will increase, thus necessitating portable and user-friendly CSTDs. Although CSTDs are mainly utilized in oncology, their usage is being broadened to other therapeutic areas, such as rheumatology, neurology, and infectious disease therapy. Wider use of CSTDs for the management of hazardous drugs across different therapeutic areas will further drive U.S. closed system transfer devices market growth.

Published by Sanket Gokhale , February 2025

For any questions about this dataset or to discuss customization options, please write to us at sales@statifacts.com

| Stats ID: | 7983 |

| Format: | Databook |

| Published: | February 2025 |

| Delivery: | Immediate |

| Price | US$ 1550 |

| Stats ID: | 7983 |

| Format: | Databook |

| Published: | February 2025 |

| Delivery: | Immediate |

| Price | US$ 1550 |

Unlock unlimited access to all exclusive market research reports, empowering your business.

Get industry insights at the most affordable plan

Stay ahead of the competition with comprehensive, actionable intelligence at your fingertips!

Learn More

Download

Download